|

Table of Contents

Volume Weighted Average Price (VWAP)

Introduction

Volume-Weighted Average Price (VWAP) is exactly what it sounds like: the average price weighted by volume. VWAP equals the dollar value of all trading periods divided by the total trading volume for the current day. The calculation starts when trading opens and ends when it closes. Because it is good for the current trading day only, intraday periods and data are used in the calculation.

Tick versus Minute

Traditional VWAP is based on tick data. As one can imagine, there are many ticks (trades) during each minute of the day. Active securities during active time periods can have 20-30 ticks in one minute alone. With 390 minutes in a typical stock exchange trading day, many stocks end up with well over 5000 ticks per day. There are over 5000 stocks traded every day and these ticks start adding up exponentially. Needless to say, tick-data is very resource intensive.

Instead of VWAP based on tick data, StockCharts.com offers intraday VWAP based on intraday periods (1, 5, 10, 15, 30 or 60 minute). Note that VWAP is not defined for daily, weekly or monthly periods due to the nature of the calculation (see below).

VWAP Calculation

There are five steps involved in the VWAP calculation. First, compute the typical price for the intraday period. This is the average of the high, low, and close: {(H+L+C)/3)}. Second, multiply the typical price by the period's volume. Third, create a running total of these values. This is also known as a cumulative total. Fourth, create a running total of volume (cumulative volume). Fifth, divide the running total of price-volume by the running total of volume.

Cumulative(Volume x Typical Price)/Cumulative(Volume)

The example above shows 1-minute VWAP for the first 30 minutes of trading in IBM. Dividing cumulative price-volume by cumulative volume produces a price level that is adjusted (weighted) by volume. The first VWAP value is always the typical price because volume is equal in the numerator and the denominator. They cancel each other out in the first calculation. The chart below shows 1-minute bars with VWAP for IBM. Prices ranged from 127.36 on the high to 126.67 on the low for the first 30 minutes of trading. It was actually a pretty volatile first 30 minutes. VWAP ranged from 127.21 to 127.09 and spent its time in the middle of this range.

Characteristics

Like moving averages, VWAP lags price because it is an average based on past data. The more data there is, the greater the lag. A stock has been trading for some 331 minutes by 3:00 PM. As a cumulative “average”, this indicator is akin to a 330 period moving average. That is a lot of past data. The 1-minute VWAP value at the end of the day is often quite close to the ending value for a 390-minute moving average. Both moving averages are based on the 1-minute bars for that day. At the close, both are based on 390 minutes of data (one full day). One cannot compare the 390-minute moving average to VWAP during the day though. A 390-minute moving average at 12:00 PM will include data from the previous day. VWAP will not. Remember, VWAP calculations start fresh at the open and end at the close. 150 minutes of trading have elapsed by 12:00 PM. Therefore, VWAP at 12:00 PM would need to be compared with a 150-minute moving average.

Despite this lag, chartists can compare VWAP with the current price to determine the general direction of intraday prices. It works similar to a moving average. In general, intraday prices are falling when below VWAP and intraday prices are rising when above VWAP. VWAP will fall somewhere between the day's high-low range when prices are range bound for the day. The next three charts show examples of rising, falling and flat VWAP.

Uses for VWAP

VWAP is used to identify liquidity points. As a volume-weighted price measure, VWAP reflects price levels weighted by volume. This can help institutions with large orders. The idea is not to disrupt the market when entering large buy or sell orders. VWAP helps these institutions determine the liquid and illiquid price points for a specific security over a very short time period.

VWAP can also be used to measure trading efficiency. After buying or selling a security, institutions or individuals can compare their price to VWAP values. A buy order executed below the VWAP value would be considered a good fill because the security was bought at a below average price. Conversely, a sell order executed above the VWAP would be deemed a good fill because it was sold at an above average price.

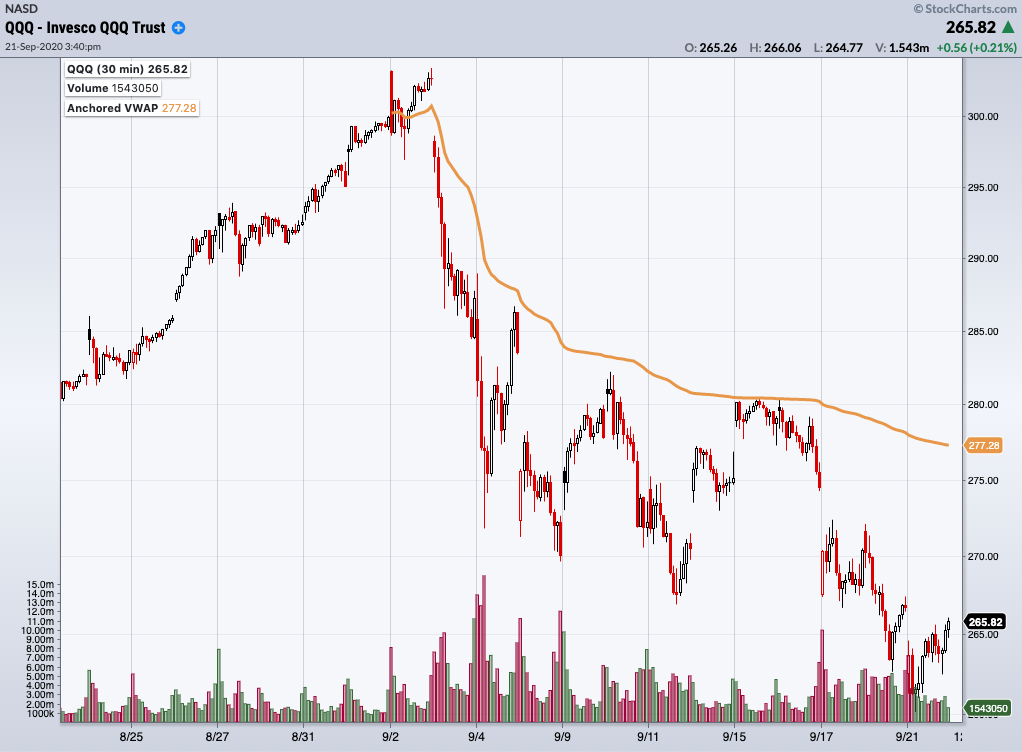

Anchored VWAP

While traditional VWAP starts at the first bar of the day and ends at the last bar of the day, Anchored VWAP allows the chartist to choose their own starting bar. The overlay is typically started at a significant high or low, earnings announcement, or some other indicator of a change in market psychology. This way, VWAP is calculated using only price action since the significant event occurred.

Because the starting bar is chosen by the chartist, and the ending bar is the most recent bar available, Anchored VWAP can span multiple days. Since this version of the overlay is not confined to a single trading day, Anchored VWAP can be used on daily charts as well as intraday charts.

Learn More: Anchored VWAP

Conclusion

VWAP serves as a reference point for prices for one day. As such, it is best suited for intraday analysis. Chartists can compare current prices with the VWAP values to determine the intraday trend. VWAP can also be used to determine relative value. Prices below VWAP values are relatively low for that day or that specific time. By contrast, prices above VWAP values are relatively high for that day or that specific time. Keep in mind that VWAP is a cumulative indicator, which means the number of data points progressively increases throughout the day. On a 1-minute chart, IBM will have 90 data points (minutes) by 11:00 AM, 210 data points by 1:00 PM and 390 data points by the close. The number dramatically increases as the day extends. This is why VWAP lags price and this lag increases as the day extends.

Using with SharpCharts

Volume-Weighted Average Price (VWAP) can be plotted as an “overlay” indicator on Sharpcharts. After entering the security symbol, choose an “intraday” period and a “range.” This can be for 1 day or “fill the chart.” Chartists looking for more detail can choose “fill the chart.” Chartist looking for general levels can choose 1 day. VWAP can be plotted over more than one day, but the indicator will jump from its prior closing value to the typical price for the next open as a new calculation period begins. Also, note that VWAP values can sometimes fall off the price chart. VWAP at 45.5 will show up on a chart with a price range from 45.8 to 47. Chartists sometimes need to extend the range to a full day to see VWAP on the chart. The VWAP value is always displayed at the top left of the chart. Click here to see a live example.

For more details on the parameters used to configure VWAP overlays, please see our SharpCharts Parameter Reference in the Support Center.