Table of Contents

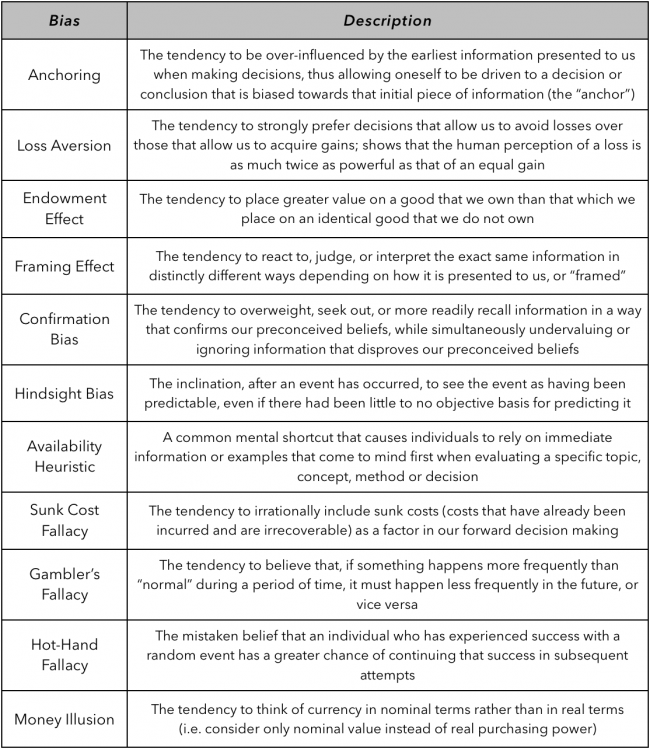

Cognitive Biases

Introduction

Central to the fields of both psychology and behavioral finance, cognitive biases describe the innate tendencies of the human mind to think, judge, and behave in irrational ways that often violate sensible logic, sound reason or good judgment. The average human – and the average investor – is largely unaware of these inherent psychological inefficiencies, despite the frequency with which they arise in our daily lives and the regularity with which we fall victim to them. While the complete list of cognitive biases is extensive, this article focuses on eleven of the most common tendencies, chosen for both their prevalence in human nature and their relevance to investing in the financial markets. The purpose of this article is to educate you on these psychological predispositions so that you can better recognize and overcome them in your own decision making.

Anchoring

Also referred to as focalism, anchoring is the tendency to be over-influenced by the earliest information presented to us when making decisions, thereby allowing oneself to be driven to a decision or conclusion that is biased towards that initial piece of information. This earliest piece of information is known as the “anchor,” the standard off of which all other alternatives are judged. Thus, subsequent decisions are made not on their own, but rather by adjusting away from the anchor.

For example, in price negotiations over a used car, the first price offered by the salesman sets the anchor point, from which all subsequent offers are based. By offering an initial price of, say, $30,000, a used-car salesman anchors the customer to that price, implementing a bias towards the $30,000 level in the subconscious of the other party. Even if the $30,000 offer is significantly above the true value of the car, all offers below that level appear more reasonable and the customer is likely to end up paying a higher price than he or she originally intended.

While the used car example may seem somewhat harmless, psychologists have captured the effects of the anchoring bias in other more significant settings. For example, researchers have shown that court decisions of judges can be swayed significantly by anchoring effects. In one setting, judges were presented with details of a court case and asked to award damages to the appropriate party. Some of the judges were provided with a low anchor (a low damage estimate) while others were provided no anchor. On average, damages awarded by judges who were given the low anchor were 29% less than those awarded by the non-anchored judges. In a similar study, judges were provided details of a case and asked to determine the duration of an appropriate prison sentence. The anchor given to the judges was set by rolling two dice on the table directly front of them. Even when the anchor was set completely randomly in this fashion and its source was witnessed by the judges, the study showed that their sentencing decisions were still subject to the anchoring effect and biased when a high dice number was rolled.

In a financial market setting, anchoring is at play anytime the estimates or expectations of another party are allowed to influence your own judgments. For example, if a price target for a stock that you are considering is set by a particularly vocal Wall Street analyst at $200.00, your own estimates for that security’s potential price movement can be easily swayed towards that figure, potentially blurring your clarity of thought, inflating your expectations and dragging you into a poor decision.

Loss Aversion and the Endowment Effect

First demonstrated by prominent psychologists Amos Tversky and Daniel Kahneman, the concept of loss aversion refers to the human tendency to strongly prefer decisions that allow us to avoid losses over those that allow us to acquire gains. Loss aversion implies, for example, that the pain one will suffer from a loss of $500 is significantly greater than the satisfaction they will receive from a gain of $500. Many studies on loss aversion commonly suggest that the human perception of loss is twice as powerful as that of gain. This forms the basis of what is known as Prospect Theory, a behavioral economics concept that describes the way in which people choose between probabilistic alternatives that involve risk. At its core, Prospect Theory shows that a loss is perceived as more significant than an equivalent gain. When graphed, the Prospect Theory value function developed by Tversky and Kahneman forms the following curve, the asymmetrical shape of which demonstrates the unequal valuing of identical gains and losses:

Loss aversion is discussed at great length not only in psychological studies of how humans make decisions, but also in the field of economics. In economics, loss aversion is a core concept at work when considering how individuals act in scenarios that involve risk. Because individuals prefer avoiding losses to achieving gains, loss aversion drives us to be risk-averse when evaluating outcomes that involve similar gains and losses.

Loss aversion was first proposed by Kahneman and his colleagues in 1990 as an explanation for a strongly related concept known as the endowment effect. The endowment effect describes the human tendency to place greater value on a good that we own than that which we place on an identical good that we do not own. Together, loss aversion and the endowment effect lead to a violation of the basic economic principle known as the Coase Theorem, which says that “the allocation of resources will be independent of the assignment of property rights when costless trades are possible”. Research has shown that even when a trade involves no cost, ownership still creates disparities in perceived value between parties due to the endowment effect.

For example, researchers have demonstrated the endowment effect by distributing a coffee mug to each participant in a study and then offering them the opportunity to sell or trade the mug for an alternative good (in this case, pens) of equal value. On average, the compensation that the participants required to part with the mug (their willingness to accept) was nearly twice as high as the amount they were willing to pay for the mug (their willingness to pay). In just a few short minutes, those participants who received a mug had ascribed ownership to the object, raising their perception of its value. Another famous study on the endowment effect found that participants' hypothetical selling price for NCAA Final Four basketball tickets was an average of 14 times greater than participants' hypothetical purchase price. Even when entirely imaginary, ownership (endowment) of the tickets fosters greater perceived value of them.

Relating the concepts of loss aversion and the endowment effect back to the financial markets, it is easy to see how these tendencies can influence an investor. Loss aversion has a distinct impact on our risk tolerance both before and after executing a trade. Combined with other cognitive biases, our tendency to steer away from loss can lead to denial as losses build in a poor position, for example, causing us to ignore weakening positions in an attempt to diminish their emotional impact. Similarly, if the endowment effect leads us to ascribe greater value to a security simply because we feel a sense of ownership over it, then that emotional attachment can lead to clouded judgment when the time comes to sell.

The Framing Effect

The framing effect describes our tendency to react to, judge, or interpret the exact same information in distinctly different ways depending on how it is presented to us, or “framed” (most commonly, whether the information is framed as a loss or as a gain). Building off of the previously discussed concepts of loss aversion and Prospect Theory, people tend to avoid risk when information is presented in a positive frame but seek risk when information is presented in a negative frame.

The most commonly cited example of this is a 1981 Tversky and Kahneman study that asked participants to choose between two treatments, A and B, for 600 people affected by a deadly disease. Treatment A was predicted to result in a guaranteed total of 400 deaths, while treatment B had a 33% chance that no one would die but a 66% chance that everyone would die. The same two alternatives were then presented to the study's participants either under a positive frame (how many peoples' lives would be saved) or under a negative frame (how many people would die).

When the alternatives were framed positively, 72% of participants chose Treatment A (“saves 200 lives”). When the exact same alternatives were framed negatively, however, only 22% of participants chose Treatment A (now presented as “400 people will die”). Saving 200 of the 600 lives is the exact same outcome as letting 400 of the 600 die, but the manner in which this identical treatment option was framed resulted in a massive decrease in the number of participants who chose it. Under the positive frame, the majority of participants avoided risk by choosing the treatment that resulted in a sure saving of 200 lives. Under the negative frame, however, the majority of participants sought the riskier alternative treatment that offered a 33% chance of saving all 600 lives.

Another famous example that demonstrates the impact of framing is a study that found 93% of PhD students registered for classes early when a penalty fee for late registration was emphasized, but only 67% did so when the same number was presented as a discount for early registration.

It is no secret that investors in the financial markets are under a constant barrage of information from all different sides - bullish, bearish, and everything in between. The exact same information can be framed by multiple sources in many different ways, biasing your interpretation of it. As you filter the stream of news and financial data that comes your way, consider the manner in which those numbers, statistics or reports are framed and think about the impact that their presentation has on the opinions they lead you to form.

Confirmation Bias

Confirmation bias is the tendency to overweight, favor, seek out, exaggerate or more readily recall information or alternatives in a way that confirms our preconceived beliefs, hypotheses or desires, while simultaneously undervaluing, ignoring or otherwise giving disproportionately less consideration to information or alternatives that do not confirm our preconceived beliefs, hypotheses or desires. This inherent flaw in our cognitive reasoning leads to misconstrued interpretations of information, errors in judgment, and poor decision making. The effects of confirmation bias have been shown to be much stronger for emotionally-charged issues or beliefs that are deeply entrenched. In addition to overvaluing information that confirms our preexisting beliefs, confirmation bias also includes our tendency to interpret ambiguous evidence as supporting existing positions, even if no true relationship exists. In short, this concept says that individuals are biased towards information that confirms their existing beliefs and biased against information that disproves their existing beliefs, leading to overconfidence in our opinions and our decisions even in the face of strong contrary evidence.

As an investor in the financial markets, it can be difficult to maintain a separation between informed estimates or expectations and emotional judgments based on hopes or desires. By causing us to overweight information that confirms such hopes or desires, confirmation bias can affect our abilities to make sound assessments and form well-reasoned opinions about, for example, a stock's upside potential. Awareness of our natural biases towards confirming information and, perhaps more importantly, our biases against disproving information is the first step in combating the unwanted effects of confirmation bias.

Hindsight Bias and the Availability Heuristic

Hindsight bias describes our inclination, after an event has occurred, to see the event as having been predictable, even if there had been little to no objective basis for predicting it. This is the psychological tendency that causes us, after witnessing or experiencing the outcome of even an entirely unforeseeable event, to exclaim “I knew it all along!”

The discovery of hindsight bias emerged during the early 1970s as the field of psychology witnessed an expansion of investigations into heuristics and biases, largely led by Amos Tversky and Daniel Kahneman. Along with the uncovering of tendencies such as the hindsight bias came the discovery of the availability heuristic, a common mental shortcut that causes individuals to rely on immediate information or examples that come to mind first when evaluating a specific topic, concept, method or decision. According to the cognitive reasoning behind the availability heuristic, if something can be recalled, it must be important, or at least more so than alternatives that are not as readily recalled. As a result, individuals tend to more heavily weight recent or immediately-recalled information, creating a bias towards the latest news, events, experiences or memories.

The Sunk Cost Fallacy

The sunk cost fallacy rests on the economic concept of a sunk cost: a cost that has already been incurred and cannot be recovered. While theoretical economics says that only future (prospective) costs are relevant to an investment decision and that rational economic actors therefore should not let sunk costs influence their decisions, the findings of psychological and behavioral finance research show that sunk costs do in fact affect real-world human decision making. Because of our tendencies towards Loss Aversion and other cognitive biases, we fall victim to the sunk cost fallacy, which describes our irrational belief that sunk costs should be considered a legitimate factor in our forward decision making when, in fact, their consideration often leads us towards inefficient outcomes.

For example, let's say a gentleman named Fred is concerned about his weight and decides to go on a diet. As part of his cleanse, he empties his fridge of all tasty temptations. When he comes across an unopened tub of ice cream, however, he falls victim to the Sunk Cost Fallacy. Even though the $15.00 Fred spent on the ice cream is a sunk cost that has already been incurred and cannot be recovered, Fred convinces himself that he cannot let the ice cream go to waste because he previously spent his hard-earned dollars to buy it. Eating a full tub of ice cream is in no way in line with his current weight-loss objectives, as the calories he will take in by consuming it are many times the daily total target of his new diet. Still, despite the adverse consequences for his health goals, Fred is swayed into eating the ice cream because of the Sunk Cost Fallacy.

In an investment setting, the consequences of the sunk cost fallacy can be much more severe than some unwanted calories. As the share price of a security falls, investors often begin to employ the logic that “I've already lost $XXX, it's too late to sell now.” As prices keep falling further and losses grow, the investor's commitment to the sunk cost continues to escalate. “Now I’ve lost $XXXXX, there's no way I can sell now. It has to come back eventually. I'll just hold on to it.” Improper or irrational considerations of sunk costs can lead to poor decisions that continue to spiral out of control, simply because of an incorrect perception of an expense that is irrecoverable.

The Gambler's Fallacy

The gambler's fallacy, also known as the Monte Carlo Fallacy, is the mistaken tendency to believe that, if something happens more frequently than “normal” during a period of time, it must happen less frequently in the future, or that, if something happens less frequently than “normal” during a period of time, it must happen more frequently in the future. This tendency presumably arises out of an ingrained human desire for nature to be constantly balanced or averaged. In situations where the event being observed or measured is truly random (such as the flip of a coin), this belief, although appealing to the human mind, is false.

The gambler's fallacy is, rather obviously, most strongly associated with gambling, where such errors in judgment and decision making are common. It can, however, arise in many practical situations, including investing. Winning and losing trades are in many ways similar to the flip of a coin and thus subject to the same psychological biases. If an investor has a series of losing trades, for example, he or she can begin to erroneously believe that, since the statistics feel unbalanced, his or her probability of making a profitable trade increases. In reality, the probability of his or her next trade being profitable is unaffected by previous losses.

The Hot-Hand Fallacy

The hot-hand fallacy is the mistaken belief that an individual who has experienced success with a random event has a greater chance of continuing that success in subsequent attempts. This cognitive bias is most frequently applied to gambling (where individuals in games such as blackjack believe that the luck they have randomly stumbled upon is actually a “hot hand” and will continue indefinitely) and sports such as basketball (where “hot” shooters see a spike in confidence after making multiple shots in a row, fueling a belief that the trend will continue throughout the rest of the game). While previous success at a skill-based athletic task, such as making a shot in basketball, can change the psychological behavior and future success rate of a player, researchers continue to find little evidence for a true “hot hand” in practice. Similar to what was discussed with the gambler's fallacy, individuals often have trouble processing or believing statistically-acceptable deviations from the average, causing them to assume that forces other than normal statistics must be at play. As an investor, a series of winning trades can induce risky overconfidence one’s “hot hand” of the moment, leading to errors in judgment and poor decision making.

The Money Illusion

In economics and behavioral finance, the money illusion describes the tendency to think of currency in nominal terms rather than in real terms. In other words, humans commonly consider money in terms of its numerical or face value (nominal value) instead of considering it in terms of its real purchasing power (real value). Because modern currencies have no intrinsic value, the real purchasing power of money is the only true (and rational) metric by which it should be judged. Still, humans often struggle to do so because, derived from all the complex underlying value systems in both domestic and international economies, the real value of money is constantly changing. In the financial markets, many average investors commonly ignore the real value of their currency when valuing their investments or interpreting their appreciation, leading to incorrect perceptions of value and past performance.

About the Author

Grayson Roze is the author of "Trading for Dummies" (Wiley, 2017) and "Tensile Trading: The 10 Essential Stages of Stock Market Mastery" (Wiley, 2016). He currently serves as the Business Manager for StockCharts.com. Grayson also speaks regularly at various investment seminars throughout the country, including to organizations such as the American Association of Individual Investors (AAII) and the Market Technicians Association (MTA). He is the co-founder of Stock Market Mastery, which provides functional investment education to individuals through multiple mediums, including live courses, books and DVDs (visit "StockMarketMastery.com" to learn more). Grayson holds a Bachelor's degree from Swarthmore College, where he studied Economics and Psychology.

Further Study

| Investing with the Trend Gregory L. Morris | Investment Psychology Explained Martin J. Pring |

|  |

| |